Family Code § 2640 reimbursement claims in Sacramento and Placer County property division cases

The short answer

Yes, usually. California Family Code § 2640 lets you recover separate property you contributed to a community asset (like a down payment from your inheritance or premarital savings) when the marriage ends. But you only get back the dollar amount you contributed, not appreciation, even if the house has doubled in value. Recovery is also capped by the available equity in the asset itself. Whether your claim succeeds depends almost entirely on whether you can trace the funds from their separate source to the asset.

You used your inheritance for the down payment on the house. Or it was the proceeds from a property you owned before the marriage. Maybe it was savings from before you ever met your spouse. Either way, the money was yours, and now you’re getting divorced and trying to figure out whether it stays yours or whether it just got absorbed into the marital estate when the deed was signed in both names.

It’s one of the most common questions in a California divorce. It’s also one where confident-sounding answers from friends, neighbors, and online forums tend to be wrong.

Here’s what’s actually true. California Family Code § 2640 protects exactly this kind of contribution. If you used separate property to acquire or improve a community asset, you have a statutory right to be reimbursed. The right has real limits, though, and you should know them before you build expectations around what you’ll walk away with. You get the dollar amount back, not appreciation. The claim is capped by the asset’s equity. And the whole thing rises or falls on whether you can trace the money from its separate source into the asset.

This guide walks through how § 2640 actually works in Sacramento and Placer County property division cases: what qualifies, what doesn’t, what tracing looks like, how to handle commingled accounts, what happens if you put the property in both names, and how § 2640 interacts with the other reimbursement doctrines that may apply at the same time.

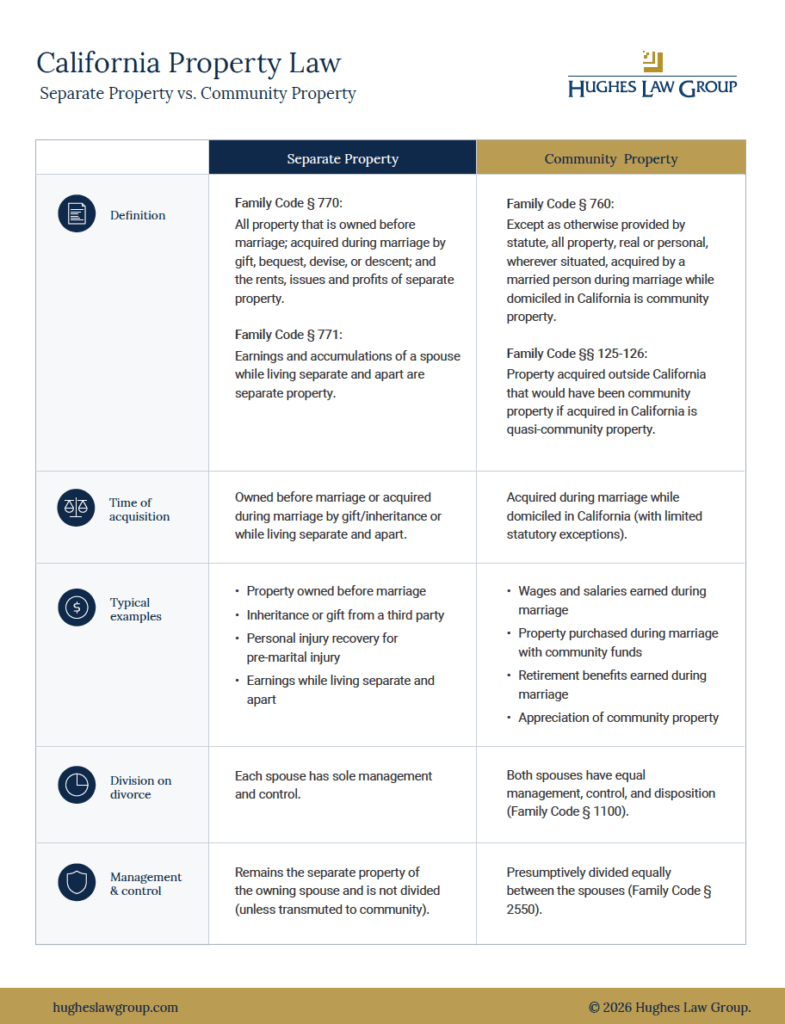

Download Our Visual Guide

Get a quick overview with our downloadable visual guide.

What Family Code § 2640 actually says

Family Code § 2640 allows a spouse to be reimbursed for separate property contributions made to community property during the marriage. The purpose is straightforward: a spouse should not lose a separate financial investment simply because it was used to acquire a jointly owned asset.

But recovery is limited. The contributing spouse is entitled only to the dollar amount contributed. There is no right to interest or appreciation unless a written agreement provides otherwise.

That single sentence disappoints more clients than almost any other rule in California family law. If you put $80,000 down on a house in 2014 from money your grandmother left you, and the house is now worth $400,000 more than you paid for it, your § 2640 claim is still $80,000. The appreciation belongs to the community, and your spouse will be entitled to half of it.

That’s the starting point. Now to the details that matter for your case.

The two limits that disappoint people most

Before going further into what qualifies, name the two ceilings on your recovery so you can plan around them.

You don’t get appreciation. § 2640 reimburses the dollar amount, not the present value. If you contributed $50,000 toward a home and the house has doubled, your reimbursement is still $50,000. The community gets the appreciation. The only common exception is when another doctrine like Moore/Marsden applies (see In re Marriage of Walrath), and that doctrine has its own framework.

You’re capped by available equity. The court treats § 2640 as tied to the asset itself, not as a personal judgment against your spouse. If the house has $60,000 of equity, a $100,000 reimbursement claim is going to be reduced. If the property is underwater, the claim may have no present value at all.

These two ceilings together can shrink a reimbursement that looked enormous on paper. Knowing this upfront changes how you should value settlement positions and how aggressively to fight over a particular asset.

What kinds of contributions qualify

Courts in Sacramento and Placer County evaluate whether a contribution meets specific statutory requirements, and a knowledgeable family law attorney will tailor the analysis to how local judges apply the rules. To qualify, the contribution must be:

- Made from a separate property source,

- Traceable to the asset in question, and

- Used for acquisition or value-enhancing improvement(s).

Common qualifying contributions include down payments on a marital residence, payments that reduce mortgage principal, and improvements funded with separate property that can be shown to increase the property’s value.

Courts closely examine the source of funds. Acceptable sources typically include premarital savings, inheritances, gifts, or proceeds from separate property sales. Without clear tracing, even legitimate contributions may not be reimbursed.

What does not qualify

Not every check you wrote for the house counts. Courts distinguish between capital contributions and routine expenses.

Non-reimbursable payments include mortgage interest, property taxes, insurance, and general household expenses. These are treated as the cost of using the property, not as building an ownership stake in it. If you have a long list of monthly payments you made from separate funds and you’re expecting all of them to come back as reimbursement, expect to be disappointed. The principal portion of the mortgage payment can qualify. The rest, ordinarily, does not.

And if you can’t trace the funds to a separate property source, the claim will likely fail regardless of how clear the use was.

Tracing is the foundation of the whole claim

Judges rely heavily on financial documentation, and testimony alone is rarely sufficient.

Sacramento and Placer County divorce courts require a clear financial path showing how separate funds were used. Strong evidence often includes bank statements, escrow records, and wire transfer confirmations. The cleanest cases look like this: an inheritance check deposited into a separate account, a wire from that account directly to escrow on closing day, escrow records identifying the deposit, and a settlement statement showing it applied to the down payment. When the path is that clean, the claim usually succeeds.

When funds pass through joint accounts before reaching the asset, the analysis becomes more complex. In contested cases, attorneys frequently work with forensic accountants to reconstruct financial transactions and address commingling. Courts give significant weight to objective financial records over recollection. If your case depends on what you remember writing on a check ten years ago, you have a harder case than someone with statements and wires.

What if the funds are commingled?

Commingling does not automatically defeat a § 2640 claim, but it changes the work that has to be done. If your separate inheritance went into a joint checking account that also received community wages, and the down payment came out of that joint account, the court is going to need a reconstruction. Sometimes that’s a direct trace (the inheritance came in on a Monday and went straight out on Wednesday to escrow, with nothing else moving through). Sometimes it requires a forensic accountant applying recognized methods to demonstrate that the down payment is fairly traceable to the separate source. For more on this, see our article, Tracing Commingled Assets: How to Unmix Your Separate Property Back Out of the Community Estate.

The point is this: commingling raises the bar; it does not lower the ceiling.

What if the house is in both names?

This is one of the most common worries. You contributed the down payment from separate funds, but when you closed, the deed was signed by both of you. Did you give your contribution away?

Not automatically. Holding the property in joint title may raise questions about your intent at the time of acquisition, but it does not, on its own, eliminate your reimbursement rights. To extinguish a § 2640 claim, your spouse would need to show by credible and admissible evidence that you intended the contribution as a gift to the community, or that you waived the right in writing. Intent has to be supported. Title alone is not enough.

Can a § 2640 claim be waived?

Yes. Reimbursement rights can be waived under certain circumstances. The most common scenario involves a written agreement, such as a prenuptial or postnuptial agreement.

Courts may also examine whether the contribution was intended as a gift to the community, an issue an experienced attorney will typically address through documentation and admissible evidence. If you signed something during the marriage that touches on the property (a refinance disclosure, a transmutation document, an estate plan), it’s worth getting in front of an attorney before opposing counsel finds it first.

How § 2640 interacts with the other reimbursement doctrines

§ 2640 doesn’t sit alone. In most Sacramento and Placer County property cases, several reimbursement doctrines may apply at once, and the order in which they are applied affects the math significantly.

Moore/Marsden: Applies when community funds reduce the loan balance on separate property, potentially giving the community a proportional interest in appreciation.

Epstein credits (Family Code § 2626): May allow reimbursement when one spouse pays community obligations after separation.

Watts charges: May apply when one spouse has exclusive use of a community asset after separation. For more on these, see our article, Navigating Finances During Separation and Divorce: Understanding Epstein Credits, Watts Charges, and Offsets for Joint Expenses and Bills.

These doctrines can overlap, and careful legal analysis is essential to avoid double counting or improper offsets. A § 2640 claim handled in isolation often produces the wrong number; the same claim handled alongside the right Moore/Marsden analysis, post-separation Epstein credits, and Watts charges produces a defensible result.

What you should do

A few practical steps protect a § 2640 claim more than anything else.

Find the documents now, not later. Pull statements from the source account going back to the original deposit. If the money came from an inheritance, locate the probate paperwork. If it was a gift, locate any letters, deposit slips, or correspondence. If it came from a separate property sale, locate the closing documents. The longer you wait, the harder these are to get.

Don’t move money around right now. If your separate source account still exists, leave it alone. Don’t transfer, consolidate, or rebalance. Anything that muddies the trail makes the work harder and more expensive later.

Write down the story while you remember it. Dates, amounts, where the money came from, where it went, what was bought, who knew about it. Memory fades. The narrative you write today will help the forensic accountant tomorrow.

Don’t agree to anything about the house yet. Settlement positions that involve the family residence frequently involve unspoken assumptions about reimbursement. If you sign without understanding your § 2640 position, you may be giving up tens or hundreds of thousands of dollars without knowing it.

Get the analysis done before you negotiate. A clear number, supported by tracing, changes the conversation. A vague claim invites a discount. Both sides know this.

Common Questions About § 2640 Reimbursement

Do I need perfect records to win a § 2640 claim?

No, but courts expect a clear paper trail. In some cases, attorneys may rely on circumstantial tracing and expert analysis from a forensic accountant. The cleaner the records, the easier the claim.

Does putting the home in both names eliminate my claim?

Not automatically. Joint title may raise questions about intent, but it does not eliminate reimbursement rights without evidence of a gift or a waiver.

What happens if funds were commingled?

Commingling does not automatically defeat a claim, but it makes tracing more complex. Courts require a clear reconstruction of how separate funds were used. For more, see our article, Tracing Commingled Assets: How to Unmix Your Separate Property Back Out of the Community Estate.

Can I recover reimbursement if the property has negative equity?

Generally no. If there is no equity, the claim may have little or no practical value at that time.

Can multiple assets affect my recovery?

Yes. Courts may allocate value across the entire marital estate, and reimbursement may be satisfied through other assets in some cases.

Do I get any of the appreciation since I made the contribution?

Not under § 2640 itself. The reimbursement is the dollar amount contributed. The exception is when another doctrine such as Moore/Marsden applies to give the community (or you) a proportional share of appreciation. That’s a separate analysis.

If you have a § 2640 claim, here’s what to discuss in a consultation

If you used inheritance, premarital savings, gifted funds, or proceeds from a separate property sale to put a down payment on a marital home or to fund improvements that increased its value, your reimbursement claim depends on documentation, timing, and the strategic presentation of evidence. An experienced family law attorney will want to review the following:

- Closing documents from when you bought the house (settlement statement and deed).

- Bank statements from the source account, going back as far as possible before the contribution.

- Wire transfer confirmations or escrow receipts showing where the money landed.

- Records of any improvements you funded with separate money, including invoices, receipts, and bank records.

- A copy of any prenuptial, postnuptial, or transmutation agreements you’ve signed.

- A written summary of the story in your own words: where the money came from, where it went, and when.

Mistakes in tracing or property characterization can significantly affect the outcome of a property division. The earlier you get the analysis done, the more options you have.

Hughes Law Group provides focused representation from an experienced Sacramento divorce attorney serving clients throughout Sacramento and Placer County courts. Schedule a consultation to assess your rights and develop a strategy tailored to your financial interests and the specific facts of your case.